Just as careful monitoring of vineyard conditions in the field is foundational to successful viticulture (Figure 1), attentive monitoring of operating economics is fundamental to the success of the vineyard business. While a vineyard operation might get by for a time without monitoring economics, it cannot thrive without the manager knowing revenues, expenses, assets, and liabilities. This information is the basis for most management decisions, essential for responding to changing economic conditions, and a foundation for reliable financial forecasts.

Figure 1. Economic monitoring, like In-field monitoring, contributes to vineyard enterprise success. (Photo Source: Progressive Viticulture©)

References for Vineyard Business Monitoring

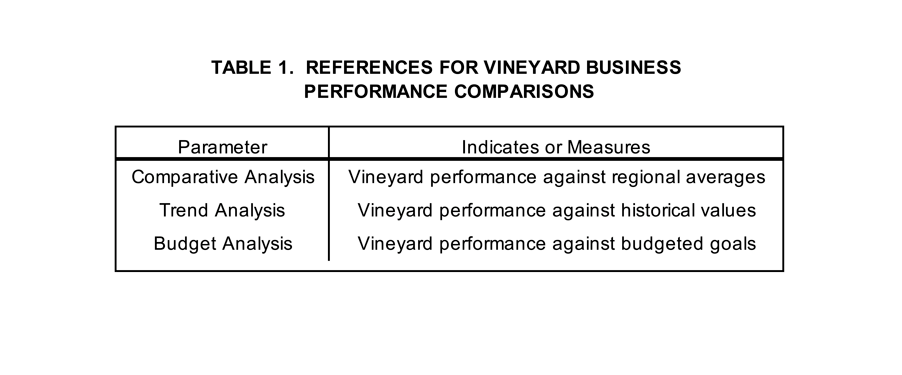

Monitoring the economic performance of a vineyard business benefits from a reference for comparison (Table 1). Among the available reference options is the University of California regional winegrape cost and return studies, which are based on local grower experiences. Some financial services, lending agencies, and other organizations provide annual record summaries for the growers they serve that can be used as monitoring references.

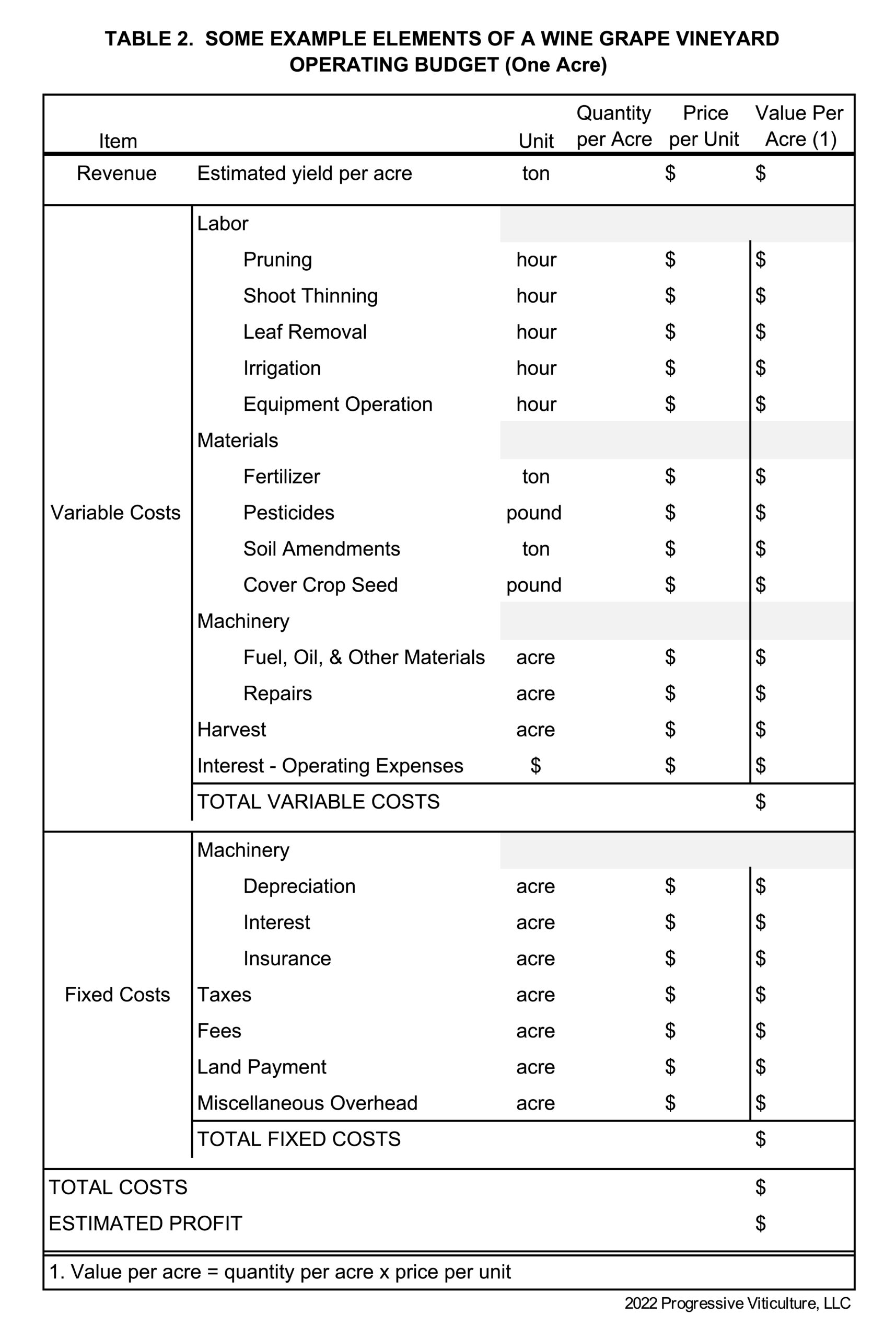

More relevant comparisons involve your specific vineyard as the reference. Comparisons of past economic performance are probably the most common. Perhaps just as meaningful are comparisons against an operating budget developed for the current growing season. The budget ought to include anticipated variable and fixed costs, as well as estimated revenues (Table 2). A budget provides a financial road map during the growing season, as well as a reference for evaluating business performance at the end.

Economic Information – The Significance of Systematic Recording

What are the requirements for effective vineyard business monitoring beyond a reference for comparison? The first is economic information that is comprehensive, accurate, and timely. To this end, record all transactions involving investment, sales, production, and other financial activities on a regular basis. For this purpose, it is often helpful to designate a specific time each week to update business records. Regular and frequent recording decreases dependence on one’s memory, which is not always reliable.

Figure 2. Computerized record keeping offers several advantages over manual record keeping. (Photo Source: Progressive Viticulture©)

The second requirement is an efficient system for storing and manipulating economic information. Fortunately, we have computers and a wide array of program options to assist us (Figure 2). Compared to manual accounting systems, computerized accounting systems greatly simplify data searches, error corrections, and report generation. They also readily incorporate double-entry record keeping that ensures debits and credits are continuously balanced. Finally, they can compute assets and liabilities on both a cost basis (purchase value) and a market basis (sales value) for balance sheets, which are discussed below. Clearly, computerization greatly enhances the value of economic records compared to manual systems.

Economic Evaluation – Reports and Analysis

The next and final steps in monitoring vineyard economics are generating and analyzing business reports. The income statement and balance sheet are the two reports most used for a business assessment. They are generated directly from accounting information. In this regard, the income statement and balance sheet are related. They differ in that the income statement is a summary of vineyard expenses and revenues over a specific period of time, while the balance sheet presents the vineyard’s financial position at a specific point in time.

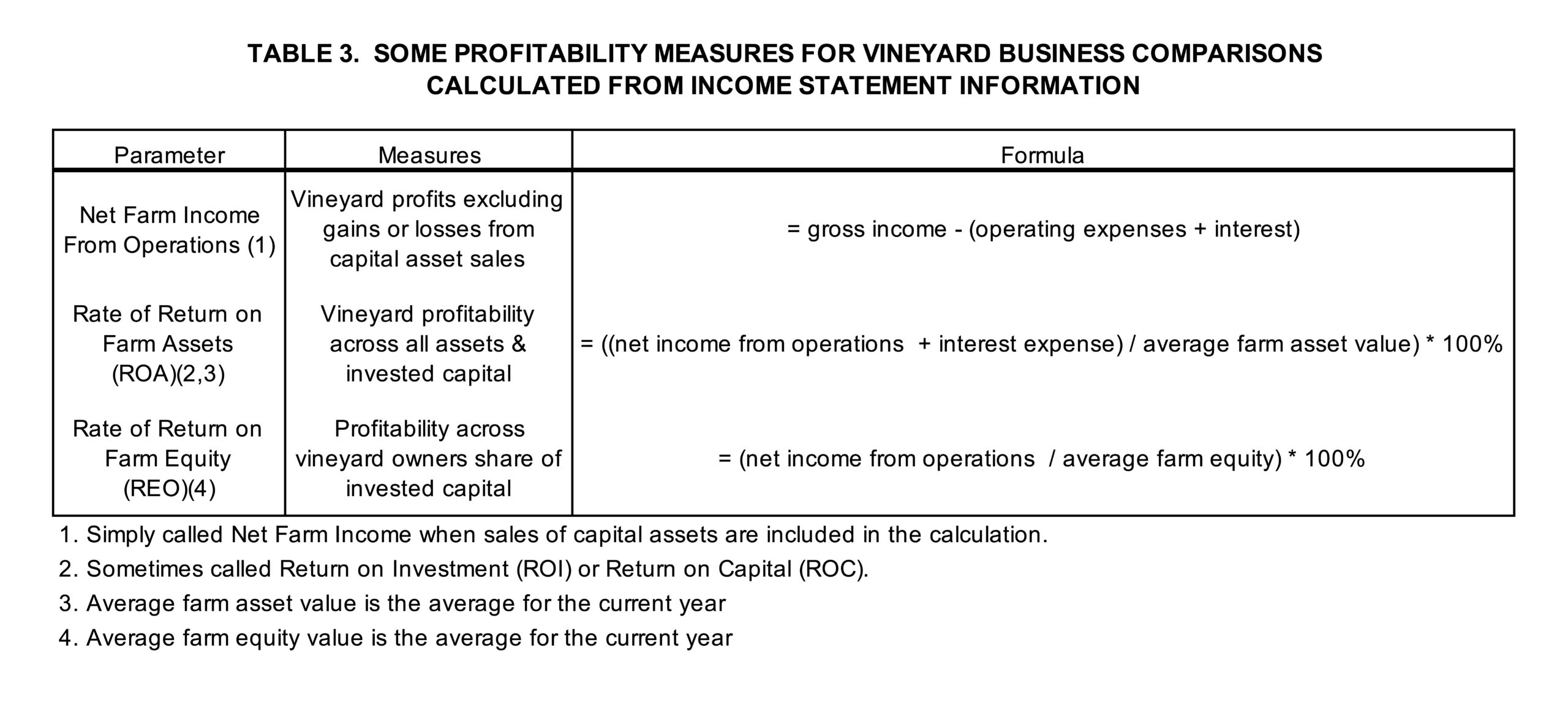

The income statement is sometimes called an operating statement or profit and loss statement. Over any specific period of time, the difference between revenues (excluding the sale of capital assets) and expenses is a vineyard’s net income from operations. The rate of return on assets and rate of return on equity are other measures of profitability, which provide additional insights into vineyard business performance (Table 3).

A balance sheet encapsulates the financial condition of a vineyard business at a specific time in terms of assets and liabilities, where anything of value a vineyard enterprise owns is an asset, and anything owed to someone else is a liability. Further, a balance sheet indicates the company’s solvency (ability to pay off liabilities), liquidity (ability to meet obligations as they come due), and net worth (equity if assets were sold and liabilities paid).

Comparative balance sheet analysis is a side-by-side examination of balance sheets from two, usually consecutive, time periods. In addition, certain calculated ratios from balance sheet values can facilitate financial monitoring over time, as well as comparisons with other vineyard enterprises, even if they differ in size (Table 4).

In Conclusion

Dr. Cliff Ohmart, former Sustainable Winegrowing Director for the Lodi Winegrape Commission, is fond of saying, “You can’t manage it if you don’t monitor it.” Fortunately, many effective tools for monitoring revenues, expenses, assets, liabilities, and other aspects of vineyard economics are available to us. It is up to us to put them to use to make informed decisions and advance the success of our vineyard businesses.

A version of this article was originally published in the Mid Valley Agricultural Services December 2013 newsletter and was updated for this blog post.

Sustainable winegrowing certification programs like LODI RULES often act like a farm business plan, plus much more. For more information, see the Business Management Chapter (Chapter 1) in LODI RULES and check out our recap of the 2017 Lodi Cost Study Customization Workshop, which has lots of helpful linked tools.

Further Reading

Beierlein, JG, Schneeberger, KC, and Osburn, DD. Principles of agribusiness management. Waveland Press, Long Grove, IL. 2008.

Grant, S. Systematic vineyard monitoring for effective vineyard management. Lodi Winegrape Commission Coffee Shop. (www.lodigrowers.com). May 03, 2021.

Grant, S. Winegrape business planning for the future. Lodi Winegrape Commission Coffee Shop. (www.lodigrowers.com). January 14, 2019.

Grant, S. The basic elements of successful vineyard management. Lodi Winegrape Commission Coffee Shop. (www.lodigrowers.com). January 26, 2018.

Grant, S. Vineyard management self-evaluation. Lodi Winegrape Commission Coffee Shop. (www.lodigrowers.com). November 18, 2013.

Grant, S. Making vineyard management decisions. Lodi Winegrape Commission Coffee Shop. (www.lodigrowers.com). December 09, 2013.

Kay, RD and Edwards, WM. Farm management. McGraw-Hill, New York. 1994.

Have something interesting to say? Consider writing a guest blog article!

To subscribe to the Coffee Shop Blog, send an email to stephanie@lodiwine.com with the subject “blog subscribe.”

To join the Lodi Growers email list, send an email to stephanie@lodiwine.com with the subject “grower email subscribe.”

To receive Lodi Grower news and event promotions by mail, send your contact information to stephanie@lodiwine.com or call 209.367.4727.

For more information on the wines of Lodi, visit the Lodi Winegrape Commission’s consumer website, lodiwine.com.

For more information on the LODI RULES Sustainable Winegrowing Program, visit lodigrowers.com/standards or lodirules.org.